#MasterclassNotes: Why distinctiveness is now a priority for marketers, agencies

At the end of 2025, a few things happened in the industry globally and locally that have made a lasting impression on all of us and which have highlighted some clear direction for agencies and marketers.

Last year was certainly an unprecedented time among the industry global networks with consolidations and acquisitions making headlines. During the last quarter of 2025, three aspects stood out for me:

The turbulence among agency networks; the sunsetting of some agency brands; the choices made in those processes

The AdForum Worldwide Summit in London in October revealed some new trends and agencies seeing things differently

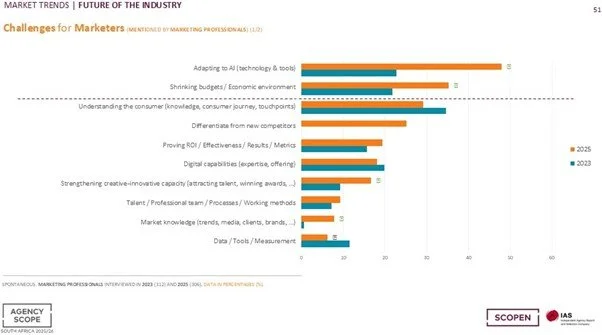

Scopen Africa’s AgencyScope South Africa results identified a new challenge for marketers, as identified by marketers themselves

Marketers are looking for agencies which will ensure that the brands they look after are distinctive and will be differentiated from any new competitors. How will marketers recognise such agencies? Those agencies will need to be distinctive and have their own strong branding that means something. Hence the growing importance of:

Clear agency positioning

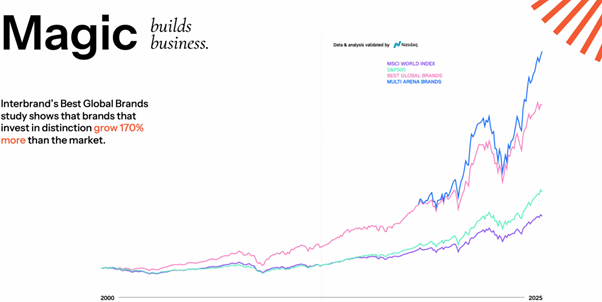

Distinctive branding: brands that invest in distinction grow 170% more than the market [see image below]

Differentiation from other competing agencies

This doesn’t mean that the other attributes aren’t still important, ie:

Knowledge of consumers

ROI

Ability to work with shrinking budgets

Adaptation to AI

So how did this change my typical face-to-face feedback presentation from AdForum Summits? Normally, I report on each of the agencies that participated but this time I highlighted the ones which stood out and were really distinctive, which I now share below (in my October 2025 column here on MarkLives, I highlighted emerging trends).

Distinctive agencies at AdForum Worldwide Summit October 2025

We met with 21 agencies at the October 2025 summit, from large network agencies to small startup agencies and established independents. The ones that stood out for their positioning and distinctiveness were as follows:

Wonderhood Studios

Wonderhood is about brand and broadcast and captivating audiences. It talked about keeping people engaged and what constitutes a good idea:

Fizz — How you react: feelings/laughter/emotion

Fame — Example of “England without immigration”

Flex — How “stretchy” is the idea? How many channels will it work in?

Wonderhood has a tool called the Captivating Coefficient. An example of captivation in action is the Waitrose Chicken case study, with 98 different assets and channels, which resulted in the highest consideration for Waitrose since 2019.

The agency is very collaborative with other agencies and oit has created “creative councils” with its clients (the larger ones) when there are many agency partners, including in-house agencies.

Publicis London — The Leo Constellation

We hadn’t seen Publicis at AdForum since 2017, so this was an important meeting. The agency team explained the history of how it’s transformed and that it’s unlike any of the other holding companies. It sees itself in a “category of one”. The group (at that time in October) was the no. 1 agency group by revenue and its client retention rate is 87% — the highest in the industry.

Leo Constellation at that point consisted of 15 000 people across 90 markets and it aspires to become the no 1 creative network globally. How will it do this?

Do the best work

Be generous — across the network

Win together

Samy

Samy is an independent agency founded in 2013, with a staff complement of 1 000 in 23 offices and 55 markets. One of the fastest-growing influencer marketing groups, it’s “end to end social”. And the name? Heart, soul and mind, and gender-free.

Social and influencer is the fastest growing sector of the advertising industry; we pitch consultants heard this several times at the summit.

Samy is a social-first agency and client comments include that “they make brands social”.

And the agency? “We make brands matter” with an intelligence-inspired creative approach, it says.

Dept

Dept describes itself as “The Growth Invention company” as invention fuels growth.

Three key points:

How do you grow faster than the world is changing?

Consumers are moving faster than companies

Companies need growth that does more than keep up

Dept remains one of the largest independent agency groups; we pitch consultants have met them many times. It itself intends to grow by connecting its distinct five specialisms: brand and media; customer experience; commerce; tech and data; and CRM and personalisation.

Its growth-invention framework is “Discover/Invent/Grow” and the agency remains 50% tech/50% marketing. First and Fast. Partner-led.

Gut

Founded seven years ago with 10 offices, full-service creative agency Gut is very active in North and Latin America, Europe and the Far East. Its HQ is in Miami, with offices in Amsterdam, Madrid, Singapore, Brazil, Argentina etc. Its priorities are agency people first; work second; and clients third.

Its positioning is “A brave agency for brave clients”. How does it do this? Bravery is not binary; bravery is a scale. It has workshops with clients in order to see where they are on the brave scale and where they want to be. Clients often rate themselves as braver than their brands.

When Gut takes on a client, it sends a comprehensive RFI to the client as it wants information, too — it’s a two-way relationship.

In terms of awards, it’s won seven Cannes Lions Grands Prix; nine Grand Effies in seven years; and is ranked the most effective network in the world. It has some of the best case studies that I’ve seen, ever.

Coolr

Another independent social agency that was founded eight years ago, Coolr sees social as the third pillar of marketing: media, creative and social. It uses social to transform brands — positioning. It has offices in the UK and US, and has six divisions/key areas:

Strategy

Creative

Content creation

Channel management

Distribution

Analytics

Coolr is the fourth fastest growing agency internationally, according to AdWeek.

Omnicom Advertising

It wasn’t only the independents which were able to position themselves. We met with a few agencies from Omnicom Advertising Group [now Omnicom Advertising — ed-at-large] and which have continued in the new structure because they’re distinctive and differentiated:

AMV/BBDO — “We craft big ideas that people love”

Native/AMV — creator-led social

AMV/Works — B2B specialism

Lucky Generals — “A creative company for people on a mission”

VCCP

This is always a highlight of the AdForum Summits because it’s consistently brilliant and has such clear positioning. The agency has been in business for 23 years and its founder reminded us of how and why the agency was started — as a challenger agency for challenger brands. Although we see many agencies claiming to be challengers, I’ve not seen any agency in particular making this claim be distinctive or stand out.

We had a three-hour session with VCCP and so were really able to see more of it and understand it more in depth. It believes that we’re “living in an era of illusion”. This started in 2005 with Facebook but now there’s an acceleration of artificiality and an avalanche of fake. Fake news, fake reviews.

The result has been a massive collapse in institutions eg governments, media and brands.

So, what can brands do about it? Double down on real. What is VCCP doing? Three things:

Sport — creating shared experiences in sport, real shared emotions

Entertainment — shared excitement, real exclusivity, real exposure, real culture

Outdoor — VCCP identifies the new “fragility of digital” and that, as a result, brands are disappearing. Strong brands need a physical presence and there are now new frontiers in outdoor. Brands can create real moments in a real world.

IPG Media Brands (now Omnicom)

It talked about media’s third revolution.

Shifting dynamics: 50% of media spend is going through media platforms. Its well-known tool Axiom is all about the enrichment of data, and what it does is add real consumer data into media-buying costs and creates margin, as well as helping to target the consumer more accurately. As a result, Media Brands sees the cost of FTEs coming down, while the cost of media will increase but through real enrichment.

Integration at last: 25% of major pitches are now fully integrated — media and creative. This is already causing media and creative agencies to move together in a more connected way, whether through the holding company (holdco) or connected network.

AI and the renaissance of brand: Brands are starting to move away from what the platforms (Google, Meta etc) are telling them and are relying more on their media agencies to advise them on best practice.

Artificial intelligence & standing out

AI is normative by nature and it can compound things — including the wrong things. It’s not a race to the bottom but a race to the mean ie average/aggregate. Here’s a quote from Mark Ritson: “AI will make us all masters of efficiency but slaves to mediocrity. The more we automate, the harder it will be to stand out.”

The answer to this is the brand itself, as the brand is the difference and the differentiator. AI learns best from differentiators and more variety in data and prompts. Technology is no longer the differentiator; technology has democratised many attributes. Thus:

Diversity of people + depth of data = differentiating brands

“AI no longer simply reads about your brand. It learns from it.” —Travis Schreiber, Fast Company

Conclusion

If one of the key challenges that marketers are facing is ensuring that their brands are differentiated, agencies and marketers alike will continue to look for solutions that will ensure distinction, differentiation and, ultimately, success.

You can also read this Marklives article online here